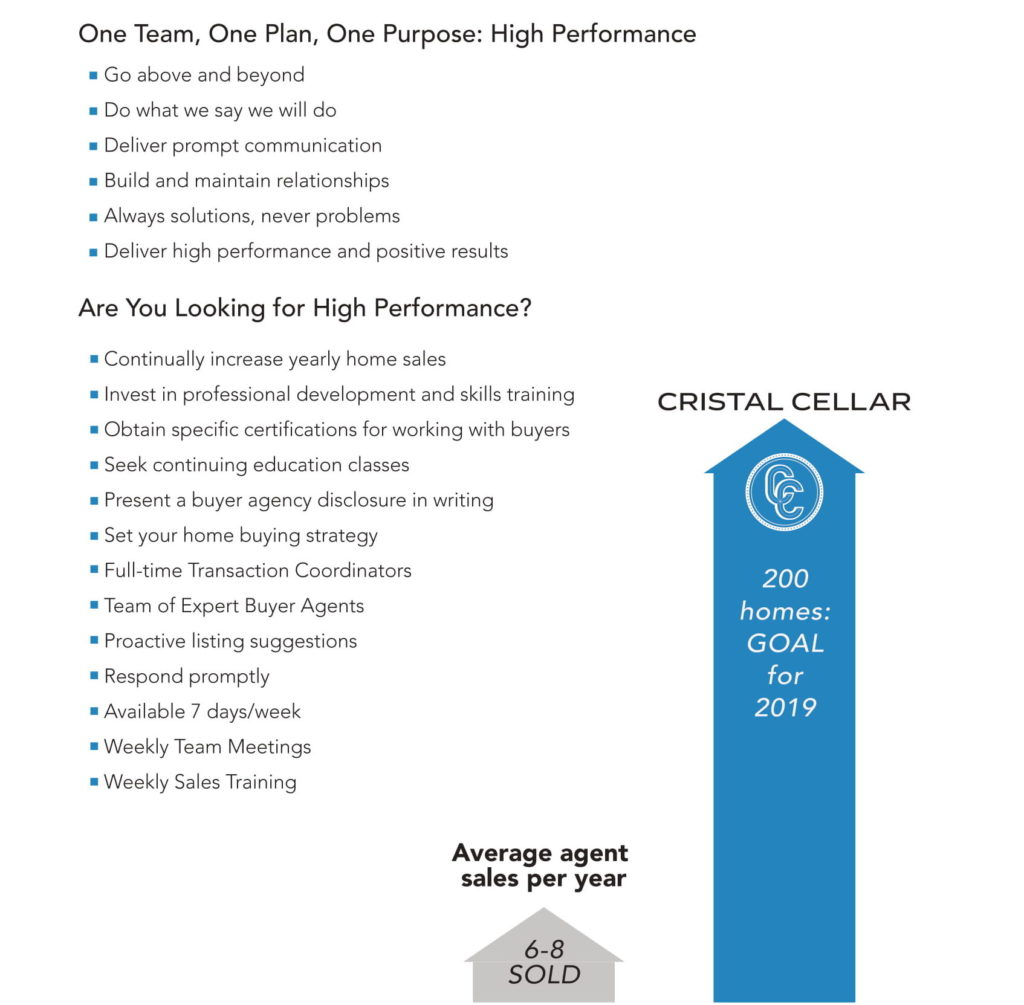

GUIDE TO THE HOME BUYING PROCESS

WHO ARE WE?

Cristal Cellar was built on the notion that the secret to achieving incredible goals and getting true results is to dominate real estate with a team approach. One part-time agent does not have the capacity to cover every aspect of the real estate process.

We operate in a supportive, professional, positive environment that helps each member of our team provide the highest level of service in the industry. This atmosphere allows our team to act on the passion and drive it takes to surpass the expectations of every client who chooses us to help fulfill their home buying or selling goals.

“...surpass the expectations of every client who chooses us...”

Whether you are looking to sell your property or buy a new home, Cristal Cellar offers a dedicated, skilled team with an innovative marketing approach.

Our team of experienced, full-time real estate agents and staff are ready to lead and advise you through the process of buying the perfect home or selling your existing home for the most amount of money in the shortest amount of time.

Vision Statement

Our vision is to grow our company by quality, not quantity, and to revolutionize the industry through creative synergy and become the premier standard for a holistic approach in the residential real estate market.

Core Values

- Loyalty

- Creativity

- Grit

Value Proposition

Our greatest value for clients is to empower them through knowledge by combining the mortgage process seamlessly with the sale or purchase of the residential real estate.

Mission Statement

The mission of Cristal Cellar is to be the first choice in the real estate and mortgage industry by building long lasting relationships.

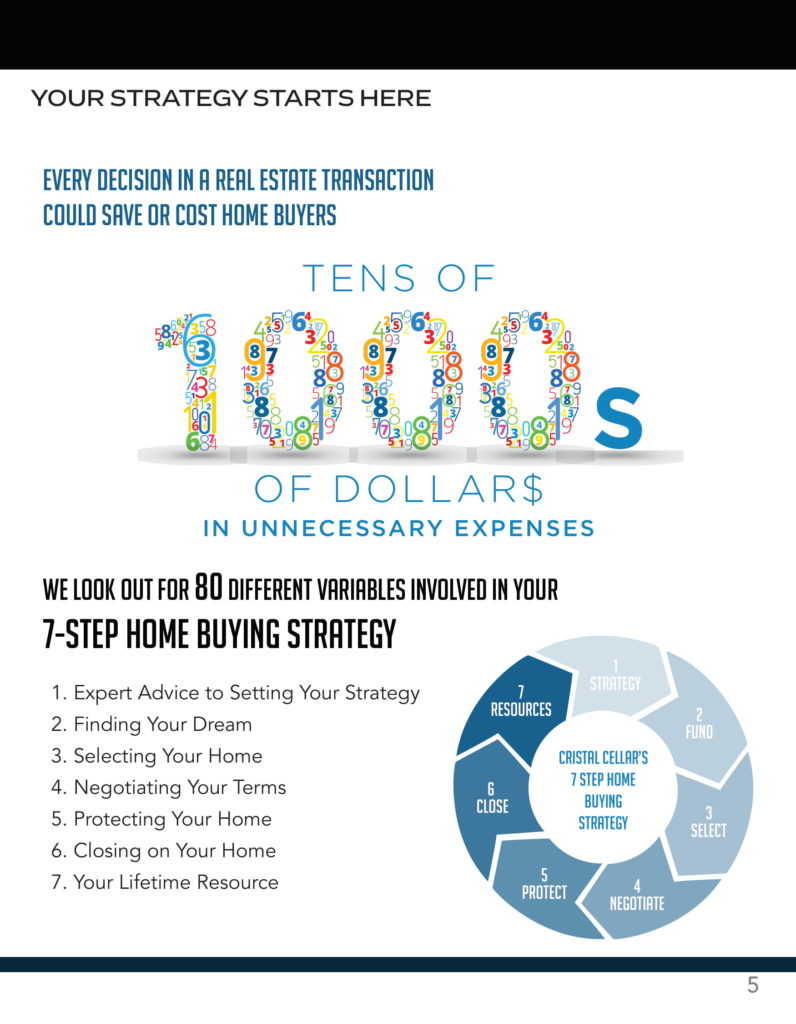

HOME BUYING ROAD MAP

YOUR STRATEGY STARTS HERE

EXPERT ADVICE FOR SETTING YOUR STRATEGY

Market Intelligence

- Economic indicators

- Trends analysis

- Interest rates

- Loan programs and qualifications

- Real estate cycles

- Seasonal advantages

- Local market conditions Micro

- markets

- National market conditions

- Absorption analysis

- Inventory of corporate-owned

- homes

- Inventory of short sales

- Inventory of foreclosures

Smart Home Buying Strategy

- Determine timing & motivation

- Evaluate needs & wants

- Out-of-pocket expenses

- Financing needs & pre-approval

- Neighborhood & lifestyle

- Quality of life

- Set expectations

- according to market

- Customized plan

- Inventory of vacant homes

- Rental housing vacancy rates

- Builder confidence

- Shadow inventory

- Inventory fluctuation

- Rent vs. buy trends

- Market stability

- Knowledge of co-op agents

- negotiation strategy

- Knowledge of mortgage options

- Knowledge of insider deals

- Knowledge of appreciation rates

- Knowledge of inventory

FUNDING YOUR DREAM

Trusted Lenders

- Best rate & terms

- Close on time

- No surprises

- Over deliver vs. Over promise

- Get documents on time to the closing attorney

Your Home as an Investment

- Mistakes that cause you to overpay

for your home - Mistakes that cause you to overpay

for your loan - How to accelerate your equity

and build wealth with

your home purchase - Why choosing the right lender makes all the difference

- Equity buyer vs. emotional buyer

Decisions on Cost

- 15-year vs. 30-year mortgage

- Long-term hold

- Short-term hold

- Buy first or sell first

- Rental property

- 13th payment

MORTGAGE PRE-APPROVAL

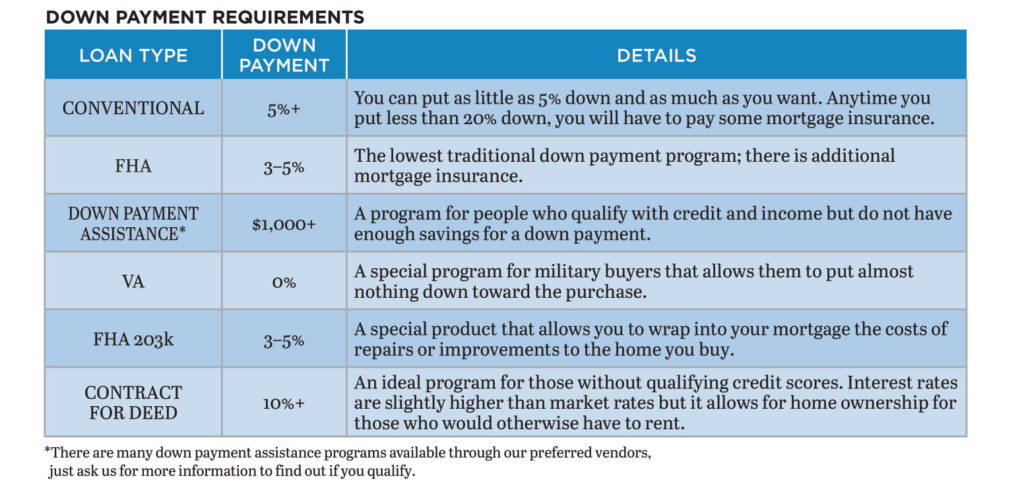

How Much Can You Afford? Key Factors to Consider

- The down payment

- The interest rate

- Credit score

- Your debt-to-income ratio

- The closing costs associated with the transaction

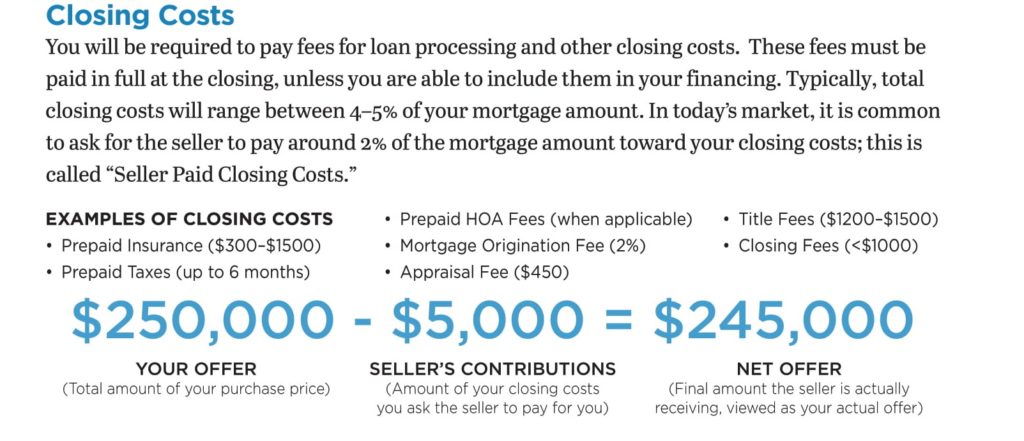

Closing Costs

You will be required to pay fees for loan processing and other closing costs. These fees must be paid in full at the closing unless you are able to include them in your financing. Typically, total closing costs will range between 4–5% of your mortgage amount. In today’s market, it is common

to ask for the seller to pay around 2% of the mortgage amount toward your closing costs; this is called “Seller Paid Closing Costs.”

SELECTING YOUR HOME

Showings

- Select homes of interest

- View your favorites

- Proactively suggest listings that match

your needs - On call “concierge” Showing Specialist

Lifestyle and Neighborhood

- School rankings

- Crime level

- Demographics

- Planned community

- Parks & playgrounds

- Privacy of neighborhood/gated

community - Location of home in neighborhood

- Proximity to: work, restaurants,

recreation, public transportation,

major roads, entertainment, etc.

Right Price — Right Home

- Property type (condo, townhouse,

single family, manufactured, multiunit,

investment) - Preferred sub divisions

- Price range

- Year built (age of home)

- Bedroom/bathroom/garage needs

- Square footage

- Landscape/lot preference

- Floor plan

- Amenities

- ADA disability features

- Appliances

Managing Risk

- Foreclosures/bank owned homes

- Short Sales

- Vacant homes

- City inspections

TYPES OF HOME SALE TRANSACTIONS

Traditional Sale (30-60 Days)

These homes have a regular seller on the other side of the transaction. They are not “upside down” on their mortgage, meaning they don’t owe more on the home than it is worth. However, if they do, they have the cash to bring to the table to sell without negotiating with the bank. The response time on your offer from a traditional seller is usually pretty prompt (generally within 24 hours, if not less). The traditional homes are going to reflect the “market value” for a neighborhood and will usually be the highest-priced home sales in the market. They will usually be in the best condition of any homes on the market.

New Construction (Varies, typically 4–6 months unless already completed)

Brand new homes, built to your tastes and warrantied. With new construction, you get precisely what you want. New construction homes can be already built, in the process of being completed, or entirely custom.

Bank Owned Sale (30-60 Days)

A bank-owned sale is one in which the bank owns the home. Usually, the bank will own the home because the seller tried to make a short sale, and the bank wouldn’t agree to it, or the seller just decided to let the home go back to the bank by not making their payments. The bank-owned transaction is a two-party transaction, 1. Buyer 2. Bank. The listing agent is the go-between with the bank, and they really help the bank’s asset manager (the decision maker at the bank) make the decisions about the property and the pricing of the home. Bank-owned sales are almost always “As Is” sales. Bank-owned purchases are usually priced well below a comparably sized “Traditional Sale,” but they may be in poor condition and most likely need some work or cleaning done.

FSBO (30-60 DAYS)

This is selling a home directly by the owner rather than having a real estate professional representation. One of the most popular reasons owners choose to sell their homes without the help of a real estate agent is to avoid paying an agent’s commission. If the owner sells their home to a person not represented by an agent, the owner pays no commission. If a real estate agent represents the buyer, that agent may request that the owner pay them a commission (typically 3%) for bringing the buyer to them. The owner can agree to pay or refuse. The seller is not legally obligated to pay the commission. Often, if the owner refuses, the buyer will compensate their agent independently. FSBO homeowners will often market their own properties or choose to employ the services of an online marketing company or listing service.

Short sale (4+ Months)

A short sale is a home that is selling for less than the mortgage balance that is owed. This is where the term “short sale” comes from; the home sells “short” of what is owed. The seller usually sells the home because they can no longer make their payments. The short sale is a three-party transaction. There is 1. Seller 2. Buyer, and 3. Bank (or banks) involved in the sale. The process is like a traditional sale: the seller hires a real estate agent to market the home and get an offer. Still, once the seller and the buyer agree to a price, the bank then has to decide if the price is acceptable and if they will release the seller from the obligation of the debt they owe. The bank must collect all of the seller’s financial records, review the offer, and send out a third party to value the property. From there, the bank will decide whether they will accept the offer, counter the offer, or reject it. Short sales can be great deals, but the waiting time involved can be extreme and very hard on a buyer wanting to purchase quickly

NEGOTIATING YOUR TERMS

Position of Strength

- Pre-approval in hand

- Type of financing

- Negotiating with listing agent

- Comparable sales o support offer

- Seller’s purchase price per tax records

- Property tax assessment review

- Walk away leverage

Seller Concessions and Offer Details

- Seller contribution to buyer’s

closing costs - Home warranty

- Inspection repair costs

- Closing date

- Discount/buy-down points

- Ancillary closing costs

- Title policy

- 60 days no payments

- Contract acceptance

- Time line

- Property inspection time line

- Negotiate repairs

Multiple Offer Strategy

- “Dear Seller” letter

- Zero repair allowance

- Increased earnest money

- Escalation Language

- Closing date

MAKING AN OFFER

Once we’ve found the home you wish to purchase, you’ll need to determine what offer you are willing to take on the home. After all, you are the one making the payments!

Offer Terms

- Sales price

- Comparative market analysis (comps)

- Earnest money

- Financing terms

- Inspection period

- Closing date

- Personal property

- Other applicable addendum like Common Interest Community Disclosures, Short Sale Contingencies, etc.

- Seller contribution to YOUR closing costs

(if requested)

A Note about Multiple Offers

It is important to remember that the more competition there is for the home, the higher the offer will have to be, sometimes even exceeding the asking price. Remember, be realistic, but it all comes down to market value and solid comparable sales. Make offers you want the other party to sign!

PROTECTING YOUR HOME

Home Inspection

- Eliminate potential surprises

- Preemptive negotiation strategy

- Identify potential “deal killers”

- Walk-away leverage

Home Warranty

- Cover the mechanical systems and

major appliances

in the home for a year - Can save buyers thousands of dollars

- Can be paid for by the seller

- Can renew after the first year is up

Lifestyle and Amenities

- Drive time

- Location of hospitals, restaurants,

schools, gyms

Future Home Maintenance Costs

- Heating and cooling costs

- Age of appliances

- Utility costs

- Home owners association dues

- Lawn and landscape maintenance

INSPECTIONS

Home Inspections

If you are purchasing a resale property, we highly recommend that you have a professional home inspector conduct a thorough inspection. Our Inspector is exceedingly thorough and detailed to minimize surprises for you. However, the inspection is not meant to lowball the seller’s post-price negotiations, as all existing homes have minor imperfections.

The inspection is intended to report significant damage or serious problems that require repair. Your home cannot “pass or fail” an inspection. The Inspector’s job is to make you aware of recommended or necessary repairs.

THE INSPECTION WILL INCLUDE THE FOLLOWING

- Appliances

- Plumbing

- Electrical

- Heating and Air conditioning

- (depending upon the season)

- Roof and Attic (if accessible)

- Foundation

- General Structure

- Radon tests are recommended — More than

- 40% of the homes tested have gas levels

- exceeding the safe threshold set by the EPA

- Thermal imaging can reveal issues unseen in a standard visual home inspection.

COMMON PRICES for the home inspector

1500 sq ft and less . . . .$350

1500–2000 . . . . . . . . . . . .$450

2000–2500 . . . . . . . . . . . .$500

2500–3000 . .. . . . . . . . . . $550

3000+ . . . .. . .(Call for pricing)

Radon Testing .. . . . . . . $150

Pest Inspections . . . . . . . .$95

Thermal Imaging

with inspection . . . . . . . .FREE

(Must request)

without inspection . . . . . $15

The seller may be willing to negotiate the completion of repairs, or you may decide that the home will take too much work and money and rescind the offer during the inspection period.

Your inspection is a contingency to the purchase agreement and needs to be completed and repairs negotiated within the due diligence date on the purchase agreement, usually a 9–10 day period.

WARRANTIES

Previously-Owned Home Warranties

When you purchase an existing home, you can purchase warranties that will protect you against most ordinary flaws and breakdowns in significant mechanicals and appliances for at least the first year you own the home. The warranty may be offered by or negotiated with the seller, or can be purchased by you, the buyer.

New Home Warranties

When you purchase a newly-built home, the builder usually offers a warranty on things such as the quality of design, materials, and workmanship.

CLOSING ON YOUR HOME

Home Owner’s Insurance

- Highly competitive rates

- Impacts your monthly payment

Title Company/Closing Attorney

- Quality management of process

- Manage all parties in transaction

- Leverage for getting problems resolved

- Closing on time

- Protecting your interests

- Transferring ownership of property to you

The Final Details

- All documents to lender in

- timely manner

- Appraisal

- Lender repairs where applicable

- Closing & settlement review

- Potential deal killers

- Transfer of utilities

- Moving into your new home

WHAT TO EXPECT AT CLOSING

Who Will Be There?

- You, the buyer(s)

Seller(s) - Buyer’s Agent

- Listing Agent

- Closing attorney, the party representing the title company

and responsible for ensuring the title is transferred to you

What Will You Need?

- Bring a valid government-issued photo ID and a second form of

ID showing your name. - Bring a cashier’s check for your cash to close (your mortgage officer will tell you the amount prior to closing)

What Is Expected from You at the Closing?

If financing the property, your lender will require you to sign a promissory note document as evidence that you are personally responsible for repaying the loan. You will also sign all title and deed documents putting you as the official homeowner!

YOUR LIFETIME RESOURCE

On-Going Real Estate Support

- Post closing questions

- Updated market information

- Helping your friends and family

Raving Fan Club

- Parties

- Holiday give-away

(ex. Thanksgiving Pie &

Valentine’s Day) - Helpful videos

- Market snapshot

- Coupons

- Quarterly giveaways

- Moving boxes

Trusted Contractors

- Handymen

- Cleaning companies

- Carpet cleaning

- Exterior maintenance

- Painting & remodeling

- Siding/Windows/Decks

FUTURE OUTLOOK

SERVICES

Real Estate

- Listing and marketing properties to obtain the highest and best offer for sellers.

- Research, locate properties, and negotiate terms on behalf of the Buyer.

- Provide clients real estate opportunities with an ROI against inflation.

- Preserve the value of the property while generating income by securing Tenants, negotiating lease contracts, collecting rent, and maintaining the property

- Negotiate on behalf of the seller with the lender for a Short Sale Approval in addition to marketing the home to obtain the highest and best offer for the seller.

- Negotiate on behalf of Buyer with the lender for best terms for Buyer.

- Facilitate in locating lease properties for prospective Tenants in addition to locating qualified Tenants for landlords.

Mortgage

- A government-backed loan program allows clients to obtain a loan with a lower down payment.

- A loan designed only for military veterans to allow them to obtain home financing with the option of no down payment.

- Provide clients with Traditional 30, 20, 15, 10 year fixed rate loans.

- Allows people with FHA loans to refinance at a lower rate with less paperwork and simplified requirements.

- Refinance for a lower payment without having to pay for closing costs.

- Tap into your home equity and use it as a form of retirement income.

- Pull cash out from the equity in the home.

- Investment loans for investors or unconventional loan programs for clients who do not qualify for conventional loans or government-backed loans.

OUR RECORD

Real Estate

Total Sales Over Past 3 years

$77,227,155

2016

Total Gross Sales: $14,829,955

2017

Total Gross Sales: $28,202,716

2018

Total Gross Sales: $34,194,48

2019

Total Gross Sales: $47,757,339

Mortgage

Total Loans Funded Over Past 3 years

$77,227,155

2016

Total Loan Amount Funded: $8,916,395

2017

Total Loan Amount Funded: $24,849,284

2018

Total Loan Amount Funded: $12,993,972019

2019

Total Loan Amount Funded: $27,926,595

THIRD PARTY REFERENCES

Chris Barredo – State Farm Insurance Agent

State Farm Chris Barredo

chris.barredo.u50s@statefarm.com

714.739.2460

Stephen Ensberg – Attorney at Law

Law Offices of Stephen E. Ensberg

sensberg@aol.com

626.813.3744

Pratik Shah – Attorney at Law

Shah Law PC

shah@shahlawpc.com

213.761.5529

Justin Tarroza – Tax Preparer

JJT Firm, LLC

justin@jjtfirm.com

818.635.1080

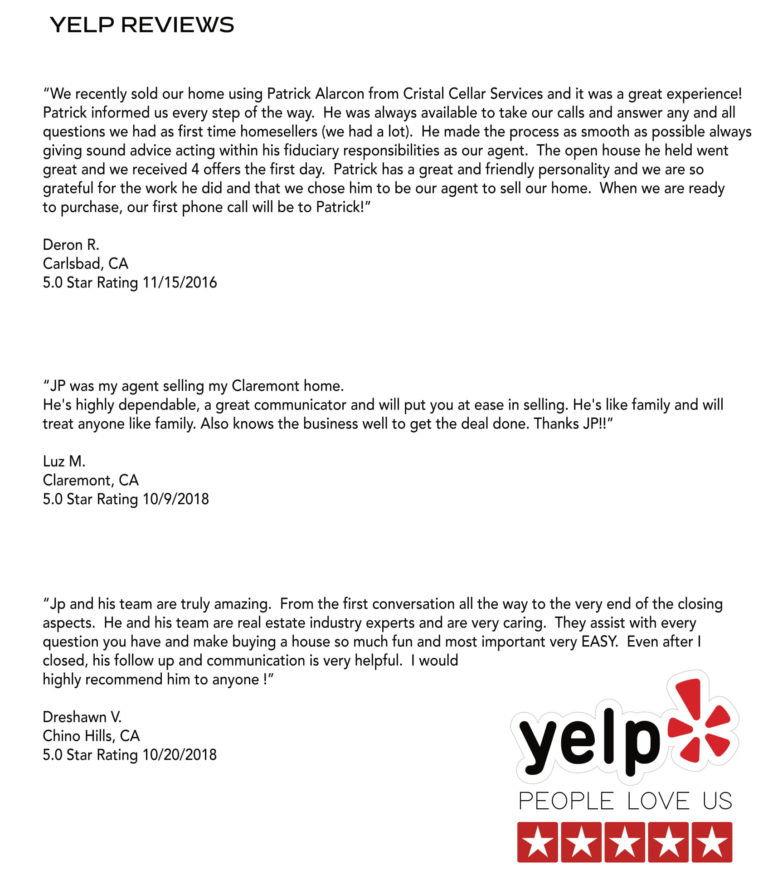

WHAT OUR CLIENTS ARE SAYING

“Exceptional service, I have worked with a couple different real estate agents in the past and although the realtors seem interested and engages in helping me find a home in the first week, their enthusiasm quickly

tapers off and they become lazy and unresponsive. JP has consistently worked with me week in and week out to make sure that I was finally able to find the home of my dreams. Whether it was sending me new

listings ever week that fit my needs to patiently showing me through multiple homes, JP truly cared about finding me the right home. I’m proud to say I finally the home of my dreams and it was due to Cristal Cellar’s consistent effort and genuine care.”

Justin P.

“As a first time home-buyer with Cristal Cellar, the services were exceptional. With a friendly and entertaining staff, their honesty and intuition have been extremely helpful. Notably, John Paul welcomed my ideas and understood my concerns.”

Chris B.